The US-Israel military offensive on Iran that began in early March 2026 has triggered a geopolitical and economic shock whose effects extend far beyond the Persian Gulf — reaching directly into Kenya’s tea-growing highlands and the Mombasa auction floor. Kenya earned Ksh 181.69 billion in 2024 from tea exports, with over 60% of that revenue flowing through markets now directly threatened by the conflict. This analysis applies the Gravity Model of Trade, Supply Chain Shock Theory, Exchange Rate Pass-Through economics, and Geopolitical Risk Premium analysis to map the full transmission of this war into Kenya’s tea sector — and prescribes the structural response that policymakers, the Tea Board of Kenya, KTDA, and farmers themselves can no longer afford to defer.

A War Tea Farmers Did Not Choose — But Cannot Ignore

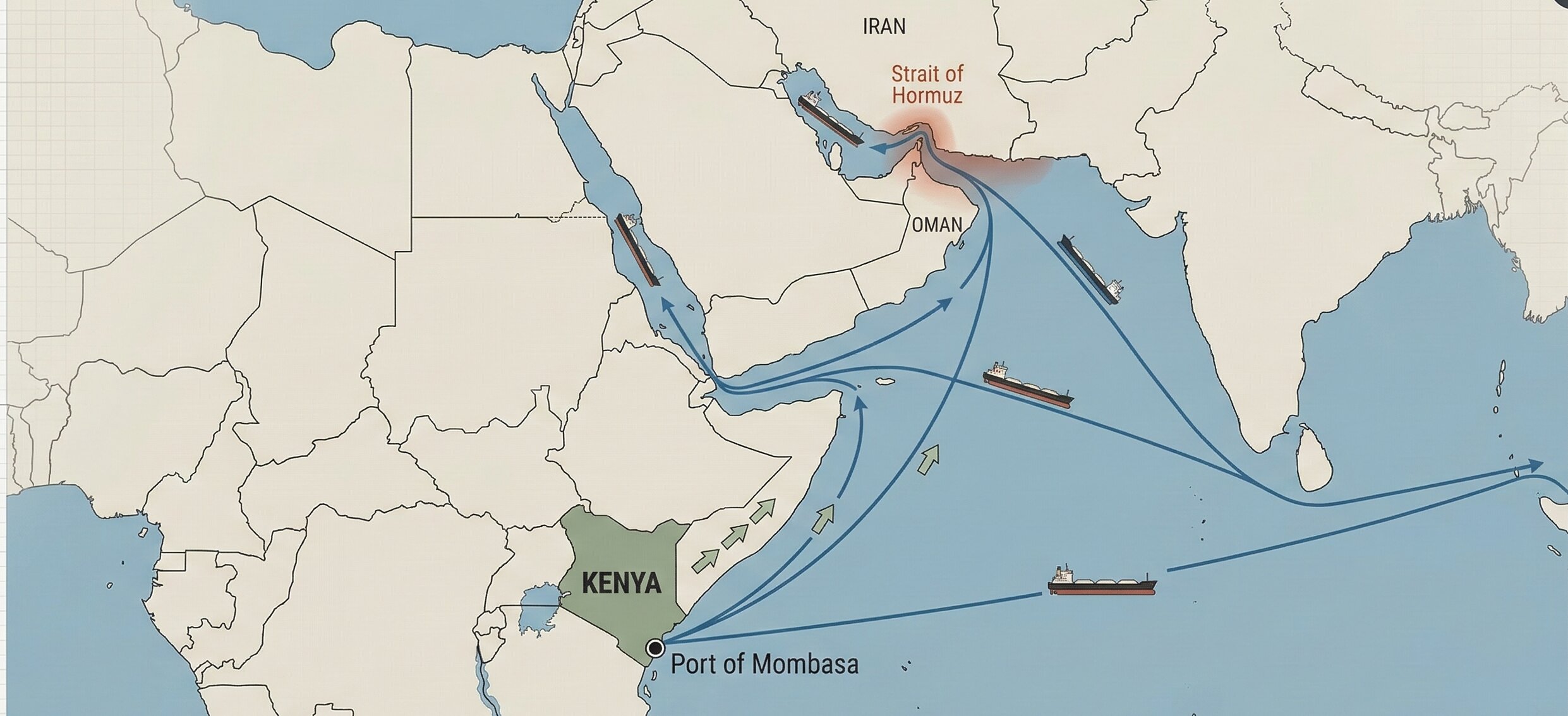

On the morning of 1st March 2026, US and Israeli forces launched coordinated military strikes on Iran, killing Supreme Leader Ali Khamenei and triggering a regional military escalation of a magnitude not witnessed since the Gulf War of 1991. Global commodity markets responded immediately: Brent crude surged 13% in the first trading session to USD 82 per barrel, natural gas futures spiked over 40%, and marine war-risk insurance was withdrawn for vessels transiting anywhere near the Persian Gulf. The Strait of Hormuz — through which 20% of the world’s daily seaborne oil supply passes — became, overnight, a conflict zone.

Kenya was not consulted. Kenya is not a party to this conflict. And yet Kenya is not insulated — not by geography, not by its stated neutrality, and certainly not by the current architecture of its tea export sector. This country earns Ksh 181.69 billion annually from tea, supports over 7 million livelihoods across the value chain, and routes more than 60% of its tea export revenue through markets that are either directly at war, geographically adjacent to the conflict, or logistically exposed through the now-threatened Strait of Hormuz. That is not a peripheral risk. It is a core systemic vulnerability — one that demands urgent, data-anchored analysis and an equally urgent policy response.

The Anatomy of Exposure: Where Kenya’s Tea Revenue Actually Lives

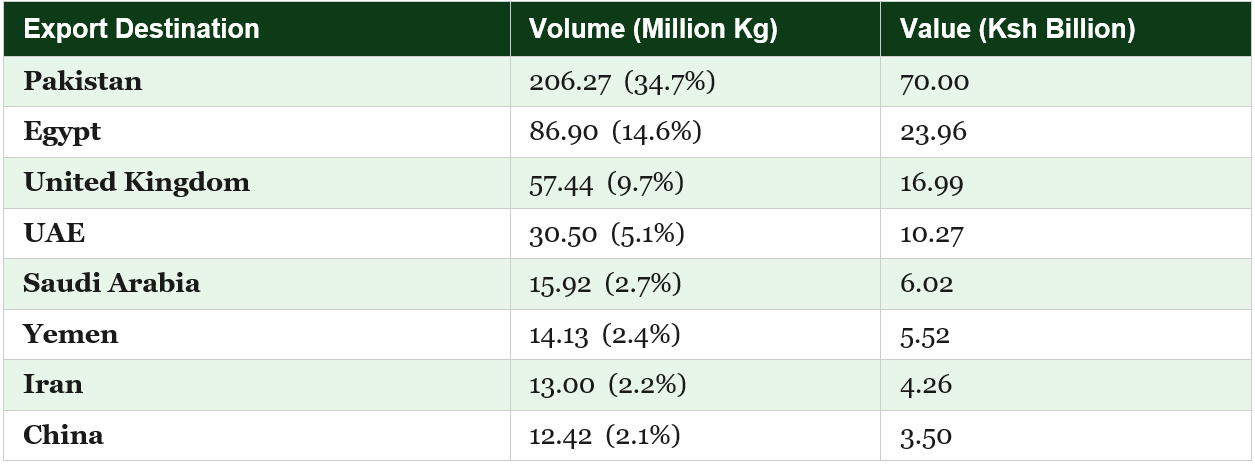

Sound economic analysis begins not with opinion but with data. Kenya exported 594.5 million kilograms of tea in 2024, generating Ksh 181.69 billion in foreign exchange — accounting for 16.3% of Kenya’s total national export earnings. The industry is the single largest source of agricultural foreign exchange in the country. The destination breakdown tells the story of risk. Financial economists describe what the table below reveals as portfolio concentration risk — the danger that arises when a large share of revenue is clustered within a single correlated risk zone. Pakistan (34.7%), UAE (5.1%), Saudi Arabia (2.7%), Yemen (2.4%), and Iran (2.2%) together account for nearly 47% of Kenya’s total tea export volume. These are not merely five separate markets. They are five markets within the direct or secondary economic blast radius of the same geopolitical event. Add Egypt — our second-largest market at Ksh 23.96 billion, whose economy is deeply integrated with Gulf energy flows and remittances — and the conflict’s economic shadow covers over 60% of Kenya’s annual tea earnings. Iran, specifically, is immediately lost: tea accounted for over 90% of Kenya’s exports to Tehran, and every trade channel — banking, cargo insurance, maritime routing — is now closed.

How a Waterway 4,000 Kilometres Away Reaches the Tea Farmer’s Pocket

The Strait of Hormuz is a 33-kilometre channel between Iran and Oman at the mouth of the Persian Gulf. It produces no tea and consumes no tea. Yet what happens there can determine whether a smallholder farmer in Murang’a receives Ksh 30 or less per kilogram of green leaf this quarter. The mechanism is Supply Chain Shock Theory — a framework developed from analysis of the 1973 OPEC oil embargo and formalised in post-2008 trade disruption literature. The theory holds that disruption at a critical supply chain node radiates simultaneously upstream into production costs and downstream into market access. Kenya faces both directions of this shock at the same time.

Upstream, Kenya imports over 80% of its refined petroleum products from Gulf producers. Tea production runs on diesel at every stage: green leaf collection vehicles, factory processing machines, and road freight to Mombasa. When Brent crude sustains above USD 85 per barrel — and analysts at the American Action Forum project prices could breach USD 100 under sustained conflict — Kenya’s annual petroleum import bill increases by an estimated Ksh 15 to 25 billion. This compresses factory operating margins and directly reduces the net earnings available to KTDA factories for farmer bonus distributions. KTDA payment data already showed farmers under pressure in 2024, with average export prices falling 8% from USD 2.47 to USD 2.27 per kilogram. A sustained energy shock tightens that vice materially further.

Downstream, marine war-risk insurance has been withdrawn by major international underwriters for all Gulf-bound routes. Shipping carriers are rerouting around the Cape of Good Hope, adding 15 transit days and USD 400 to USD 800 per container in additional costs. For bulk tea operating on margins already compressed to USD 2.27 per kilogram, a freight cost increase of even USD 0.07 to USD 0.10 per kilogram erodes profitability on entire consignments. This is the same mechanism the Tea Board documented during the 2024 Red Sea Houthi disruptions — the current crisis is more direct and more severe.

The Gravity Model of Trade — first formalised by Nobel laureate Jan Tinbergen in 1962 and one of the most empirically robust frameworks in international economics — explains this theoretically. The model establishes that bilateral trade flows are determined by economic mass and diminished by distance, where distance encompasses not just geography but all cost frictions, including conflict risk. When Hormuz is threatened, the effective economic distance between Mombasa and Karachi, Dubai, or Cairo expands dramatically — not in kilometres, but in dollars, days, insurance premiums, and trade finance terms. Trade contracts. The model predicts it. The market is already confirming it.

- 𝑺𝒖𝒑𝒑𝒍𝒚 𝑪𝒉𝒂𝒊𝒏 𝑺𝒉𝒐𝒄𝒌 𝑻𝒉𝒆𝒐𝒓𝒚 𝒘𝒂𝒓𝒏𝒔 𝒕𝒉𝒂𝒕 𝒅𝒊𝒔𝒓𝒖𝒑𝒕𝒊𝒐𝒏 𝒄𝒐𝒔𝒕𝒔 𝒓𝒊𝒔𝒆 𝒇𝒂𝒔𝒕 𝒂𝒏𝒅 𝒇𝒂𝒍𝒍 𝒔𝒍𝒐𝒘. 𝑲𝒆𝒏𝒚𝒂 𝒊𝒔 𝒂𝒃𝒔𝒐𝒓𝒃𝒊𝒏𝒈 𝒂 𝒔𝒊𝒎𝒖𝒍𝒕𝒂𝒏𝒆𝒐𝒖𝒔 𝒖𝒑𝒔𝒕𝒓𝒆𝒂𝒎 𝒑𝒓𝒐𝒅𝒖𝒄𝒕𝒊𝒐𝒏 𝒄𝒐𝒔𝒕 𝒔𝒉𝒐𝒄𝒌 𝒂𝒏𝒅 𝒅𝒐𝒘𝒏𝒔𝒕𝒓𝒆𝒂𝒎 𝒅𝒆𝒎𝒂𝒏𝒅 𝒄𝒐𝒍𝒍𝒂𝒑𝒔𝒆 — 𝒃𝒐𝒕𝒉 𝒕𝒓𝒊𝒈𝒈𝒆𝒓𝒆𝒅 𝒃𝒚 𝒕𝒉𝒆 𝒔𝒂𝒎𝒆 𝒆𝒗𝒆𝒏𝒕, 𝒃𝒐𝒕𝒉 𝒇𝒆𝒆𝒅𝒊𝒏𝒈 𝒊𝒏𝒕𝒐 𝒕𝒉𝒆 𝒔𝒂𝒎𝒆 𝒇𝒂𝒓𝒎𝒆𝒓’𝒔 𝒃𝒐𝒏𝒖𝒔 𝒑𝒂𝒚𝒎𝒆𝒏𝒕.

Our Biggest Market, Pakistan, Is Also Our Most Dangerous Dependency

No market in Kenya’s tea portfolio carries more weight — or concentrates more risk — than Pakistan. At 206.27 million kilograms and Ksh 70 billion in 2024, Pakistan commands a 34.7% share of total export volume. To contextualise: Pakistan alone buys more Kenyan tea than the United Kingdom, UAE, Saudi Arabia, Yemen, Iran, and China combined. This is not a trade relationship. It is a structural dependency — and this conflict has placed it under direct, measurable threat.

The transmission channel runs through energy economics. Pakistan is a major importer of Gulf oil and natural gas. A sustained rise in global energy prices worsens Pakistan’s chronic current account deficit, depletes its foreign exchange reserves, and places depreciation pressure on the Pakistani Rupee. Exchange Rate Pass-Through theory predicts that when the Rupee weakens against the US dollar, the local-currency cost of dollar-denominated imports rises accordingly. Tea purchased at Mombasa is priced in US dollars. Pakistani importers paying in Rupees face a dual squeeze: higher auction prices for tea and fewer Rupees to buy each dollar needed to pay for it. The net effect is reduced purchasing volume — and reduced purchasing volume means a direct decline in Kenya’s most critical revenue stream.

This is not speculative. In 2024, Pakistan’s tea purchases from Kenya declined 2% following a domestic sales tax adjustment by Pakistan’s Federal Board of Revenue. A decision made in Islamabad translated immediately into measurable volume losses at Mombasa. A 10% contraction in Pakistani tea purchases costs Kenya Ksh 7 billion annually. A 20% contraction erases Ksh 14 billion. These numbers are not outliers. They represent the central range of outcomes under conditions already developing in real time.

The Mombasa Auction: Where Geopolitics Becomes a Price

The EATTA auction in Mombasa is the pricing engine for the vast majority of Kenya’s tea. Its mechanics are governed by classical commodity market microeconomics: supply and demand meet weekly, prices clear at whatever level buyers and sellers agree, and there is no administered price floor to protect sellers when demand weakens. Geopolitical Risk Premium Theory — grounded in international finance literature — establishes that when a trade corridor becomes associated with active conflict, all rational economic actors embed a risk premium into every transaction in that corridor. Buyers reduce order volumes. Logistics firms raise rates. Banks tighten trade finance. Insurers withdraw cover. The cumulative effect is a contraction of effective demand at the auction — and lower prices for every seller.

The specific mechanism is what economists call an auction overhang. When Gulf buyers reduce bids or temporarily exit Mombasa — as UAE, Saudi, and Yemeni buyers are already doing — unsold lots accumulate and are carried forward to subsequent weekly auctions, where they depress clearing prices by expanding effective supply against weakened demand. This creates a self-reinforcing downward price cycle that persists well beyond the initial shock. The 2011 Arab Spring disrupted Egypt and Libya — contributing to Mombasa auction price depression lasting over 12 months. The current conflict simultaneously threatens buyers representing over 60% of export revenue. The overhang risk is correspondingly broader. One structural factor makes Kenya uniquely exposed. Kenya exports approximately 94% of its tea in unbranded bulk form, competing almost exclusively on price. Sri Lanka — our primary Mombasa competitor — exports nearly 48% of its tea in packaged, branded form at an average USD 5.79 per kilogram, more than double Kenya’s USD 2.27. When Gulf buyers reorient procurement under geopolitical pressure, they seek alternative suppliers who can ship through routes unaffected by Hormuz disruption. A Sri Lankan or Indian supplier offering branded, packaged tea via the Pacific or around the Cape is a materially better proposition for a risk-averse Gulf procurement manager than bulk Kenyan commodity tea delivered through a conflict zone. Kenya has almost no brand loyalty buffer against this reorientation.

- 𝑲𝒆𝒏𝒚𝒂 𝒍𝒆𝒂𝒅𝒔 𝒊𝒏 𝒕𝒆𝒂 𝒆𝒙𝒑𝒐𝒓𝒕𝒔 𝒃𝒖𝒕 𝒕𝒓𝒂𝒊𝒍𝒔 𝒊𝒏 𝒓𝒆𝒗𝒆𝒏𝒖𝒆𝒔.

The Exchange Rate Trap: When Shilling Weakness Is Not Good News

A common assumption in trade economics holds that currency depreciation benefits exporters: a weaker shilling means dollar-denominated export earnings convert to more shillings, improving local-currency revenues. This assumption, theoretically valid in isolation, breaks down precisely when production cost structures are simultaneously under pressure — which is exactly Kenya’s current condition. Exchange Rate Pass-Through economics requires us to examine both sides of the profit equation, not just the revenue line.

The oil import bill increase triggered by this conflict requires Kenya to mobilise significantly more US dollars, increasing dollar demand and placing depreciation pressure on the shilling from its current Ksh 129 per dollar. Were the shilling to weaken to Ksh 140, a tea exporter earning USD 1 million would receive Ksh 140 million instead of Ksh 129 million — an apparent gain. However, production costs — fertiliser, agrochemicals, diesel, factory maintenance, road freight — are denominated in shillings but driven by dollar-priced imported inputs. As the shilling weakens, the shilling cost of these inputs rises proportionally. The apparent revenue gain is partially or wholly offset by the simultaneous rise in production costs. For KTDA smallholder factories, where farmer payment rates are set after deducting operational costs, the squeeze is particularly acute: the depreciation benefit flows partly to exporters, while the cost increase passes directly through to the factory and ultimately to the farmer’s payment.

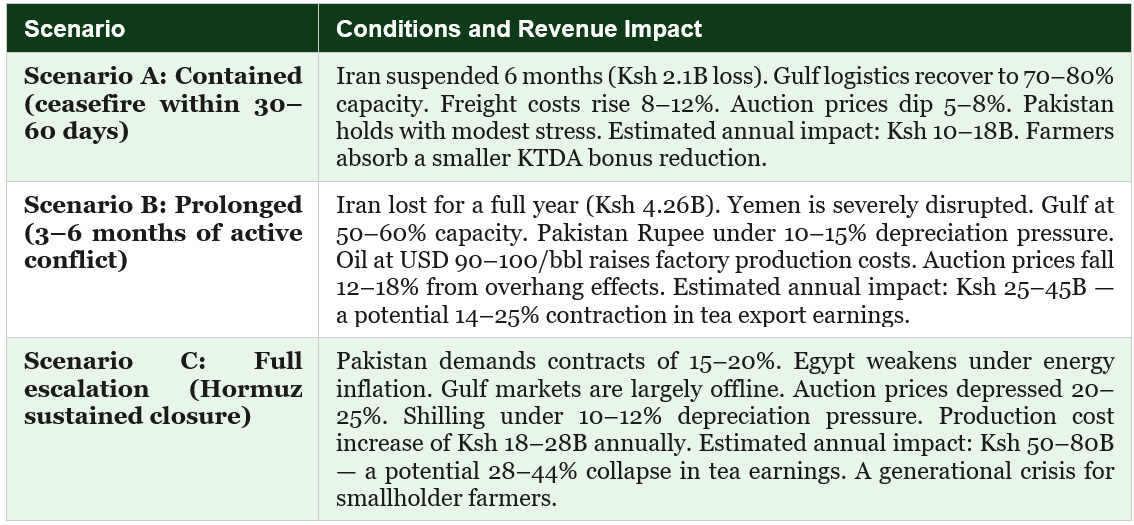

How Bad Could This Get? Three Evidence-Based Scenarios

Rigorous policy analysis requires a range of scenarios calibrated to different conflict trajectories — not a single prediction, and not a worst-case framing exercise. The following three scenarios are grounded in current geopolitical intelligence, commodity market data, and established trade shock modelling.

Even under Scenario A — the most optimistic outcome — the sector absorbs a Ksh 10 to 18 billion shock. Kenya’s tea sector was already operating under price pressure having seen average export prices fall 8% year on year in 2024. There is no comfortable scenario. There is only a range of damage, and the difference between scenarios is determined almost entirely by the speed and quality of Kenya’s policy response.

Where the Evidence Points

It is not the role of economic analysis to dictate institutional mandates. What it can do is read the data and offer a considered perspective on where it points — and in this case, the evidence points in a fairly clear direction across three horizons.

𝐈𝐧 𝐭𝐡𝐞 𝐢𝐦𝐦𝐞𝐝𝐢𝐚𝐭𝐞 𝐭𝐞𝐫𝐦, the strongest case is for better real-time intelligence — tracking auction volumes, unsold lots, freight costs, and Gulf buyer activity week by week. Exporters holding active Gulf contracts would also be well-served by examining their force majeure provisions urgently; this conflict qualifies under standard ICC trade frameworks, and the window for activating those protections is not indefinite. A convened industry conversation between tea sector bodies, financial institutions, and logistics players to map the near-term picture collectively would, in this analyst’s view, be time well spent.

𝐎𝐯𝐞𝐫 𝐭𝐡𝐞 𝐧𝐞𝐱𝐭 𝟑 𝐭𝐨 𝟏𝟐 𝐦𝐨𝐧𝐭𝐡𝐬, the data points compellingly toward market development in geographies insulated from this conflict. China, at 12.42 million kilograms in 2024 and with a domestic market structurally underserved by Kenyan tea, is the most obvious starting point. The government’s 2026 tax exemption on tea packaging materials is a well-timed instrument — the question is whether it translates into measurable acceleration of value-added exports, which at 5% of total volume remain well below their potential. Currency risk management for KTDA-linked factories is also worth serious attention; the current absence of accessible hedging instruments leaves the full force of exchange rate pass-through movements to be absorbed directly by farmer payment rates.

𝐎𝐧 𝐭𝐡𝐞 𝐥𝐨𝐧𝐠𝐞𝐫 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐡𝐨𝐫𝐢𝐳𝐨𝐧, a 34.7% single-buyer concentration in Pakistan is, by any standard portfolio risk measure, a vulnerability that this crisis has made difficult to continue deferring. What a more resilient market distribution looks like — and what instruments could credibly move toward it — seems overdue for serious, funded policy attention. A dedicated buffer mechanism capitalised from export levy surpluses in strong years, deployable during geopolitical shocks, has precedent in comparable agricultural export economies and is worth examining. The 50% value-added export target for 2027 carries a different weight now: it is not merely an industry ambition but, in light of this analysis, a meaningful structural risk reduction — one the data suggests Kenya can no longer afford to treat as optional.

A Verdict on Structural Complacency

A farmer in Kericho picking green leaf on a Wednesday morning in March 2026 has no direct connection to the missiles flying over Tehran. She has no stake in Middle Eastern geopolitics. She did not vote for any of the combatants. She is growing food, contributing to her country’s foreign exchange earnings, and hoping that the KTDA payment at month-end reflects a fair price for her labour.

But between her farm gate and that payment lies a chain of economic relationships — auction prices, freight costs, buyer demand, energy prices, exchange rates — every link of which is currently under stress because of a war she never chose. This is the modern reality of being an export-dependent agricultural economy in a globally integrated world: conflict anywhere in the trade corridor is, effectively, conflict at home.

Kenya’s tea sector has survived the 2011 Arab Spring. It has survived Red Sea Houthi disruptions. It has survived Pakistani sales tax shocks. It has survived COVID-19 freight disruptions. Its resilience is not in question. But resilience through passive endurance is not the same as strategic preparation. The sector has been surviving crises rather than designing itself out of crisis vulnerability.

The US-Israel war on Iran is, in this sense, not only a threat. It is a verdict. A verdict on 20 years of delayed value-addition reform. A verdict on the failure to diversify away from volatile Gulf markets. A verdict on the absence of financial risk management tools for smallholder-linked cooperatives. A verdict on treating geopolitical risk as someone else’s problem.

- 𝑻𝒉𝒊𝒔 𝒘𝒂𝒓 𝒉𝒂𝒔 𝒏𝒐𝒕 𝒄𝒓𝒆𝒂𝒕𝒆𝒅 𝑲𝒆𝒏𝒚𝒂’𝒔 𝒕𝒆𝒂 𝒔𝒆𝒄𝒕𝒐𝒓 𝒗𝒖𝒍𝒏𝒆𝒓𝒂𝒃𝒊𝒍𝒊𝒕𝒊𝒆𝒔. 𝑰𝒕 𝒉𝒂𝒔 𝒑𝒓𝒆𝒔𝒆𝒏𝒕𝒆𝒅 𝒕𝒉𝒆 𝒊𝒏𝒗𝒐𝒊𝒄𝒆 𝒇𝒐𝒓 20 𝒚𝒆𝒂𝒓𝒔 𝒐𝒇 𝒅𝒆𝒇𝒆𝒓𝒓𝒆𝒅 𝒔𝒕𝒓𝒖𝒄𝒕𝒖𝒓𝒂𝒍 𝒓𝒆𝒇𝒐𝒓𝒎. 𝑻𝒉𝒆 𝒒𝒖𝒆𝒔𝒕𝒊𝒐𝒏 𝒏𝒐𝒘 𝒊𝒔 𝒘𝒉𝒆𝒕𝒉𝒆𝒓 𝒑𝒐𝒍𝒊𝒄𝒚𝒎𝒂𝒌𝒆𝒓𝒔 𝒑𝒂𝒚 𝒊𝒕 — 𝒐𝒓 𝒍𝒆𝒕 𝒕𝒉𝒆 𝒇𝒂𝒓𝒎𝒆𝒓 𝒑𝒂𝒚 𝒊𝒕 𝒊𝒏𝒔𝒕𝒆𝒂𝒅.

Kenya Tea Sector — War-Risk Exposure Indicators (March 2026)

Implications by Stakeholder

𝐅𝐎𝐑 𝐓𝐄𝐀 𝐅𝐀𝐑𝐌𝐄𝐑𝐒: Bonus Pressures Are Likely in the Near Term

The evidence suggests that reduced Gulf buyer demand, combined with rising factory production costs driven by energy price pass-through, will weigh on KTDA payment rates over the next few months. How much depends on how quickly the sector responds to the market shift, and how the conflict evolves.

𝐆𝐎𝐕𝐄𝐑𝐍𝐌𝐄𝐍𝐓 & 𝐏𝐎𝐋𝐈𝐂𝐘𝐌𝐀𝐊𝐄𝐑𝐒: The Data Points Toward Early Engagement

The analysis suggests that early, coordinated engagement across the tea value chain — bringing together sector bodies, financial institutions, and logistics players — is likely to yield better outcomes than reactive responses after quarterly data confirms the damage. The window for managed adjustment is available now.

𝐓𝐄𝐀 𝐁𝐎𝐀𝐑𝐃 & 𝐊𝐓𝐃𝐀: Real-Time Market Intelligence Has Rarely Mattered More

The evidence points to significant value in close tracking of auction volumes, unsold lot accumulation, freight cost trends, and Gulf buyer participation levels over the coming weeks. Visibility into these indicators early is what distinguishes a managed adjustment from a reactive one- such will prevent task force appointments in future on taxpayers bill.

𝐄𝐗𝐏𝐎𝐑𝐓𝐄𝐑𝐒: Contract Provisions and Market Diversification Deserve Urgent Attention

Exporters with active Gulf contracts would be well-served by reviewing their force majeure provisions urgently — this conflict qualifies under standard ICC trade frameworks, and that window is not indefinite. The data also points compellingly toward accelerating buyer relationships in China, Eastern Europe, and East Asia.

𝐈𝐍𝐕𝐄𝐒𝐓𝐎𝐑𝐒: Value Addition Looks Considerably More Attractive Under This Analysis

The structural case for investment in Kenyan tea packaging, branding, and processing has strengthened materially. Value-added tea commands five to six times the price of bulk and is partially insulated from Gulf demand shocks — a risk profile that looks significantly different from bulk commodity exposure at this moment.

𝐃𝐈𝐑𝐄𝐂𝐓𝐎𝐑𝐒 𝐀𝐍𝐃 𝐎𝐓𝐇𝐄𝐑 𝐒𝐓𝐀𝐊𝐄𝐇𝐎𝐋𝐃𝐄𝐑𝐒: Pakistan Concentration Merits Careful Consideration

Recent trade patterns suggest that a 10% decline in Pakistani purchases could translate into roughly KSh 7 billion in lost sector revenue. This situation highlights the importance of gradually diversifying beyond heavy reliance on Karachi, including continued exploration of direct sales channels into alternative markets.

- The author is an economist and statistician and serves as an elected director at a factory managed by the Kenya Tea Development Agency. The views expressed are solely those of the author and represent independent professional analysis; they do not necessarily reflect the official position of any institution.

Editorial Note

This analysis represents expert commentary on economic policy and political developments. All information has been fact-checked and cross-verified from reliable sources. The views expressed are based on professional analysis and independent research.