Executive Summary

Kenya's tea sector — generating Ksh 186.91 billion in export revenue in 2025 and supporting over 7 million livelihoods — faces a compounding tax burden at a moment of acute geopolitical and market fragility.

Two specific policy interventions demand rigorous scrutiny:

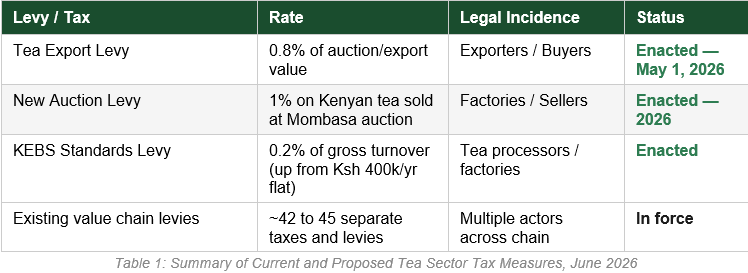

- • A 0.8% export levy on tea auction and customs value (Tea Levy Regulations, 2026, effective May 1, 2026) — legally charged to exporters but, by standard economic theory, capable of transmitting its burden backward to farmers through price compression at auction.

- • A revised KEBS Standards Levy of 0.2% of gross turnover — an escalation of up to 650% in annual compliance costs for mid-sized tea factories.

Mombasa Auction Revolt

These measures arrive simultaneously with a documented buyer revolt: within the first week of the levy's enforcement, traders at the Mombasa auction actively shifted procurement to Rwandan and Burundian teas. With 82% of tea going unsold at a recent session, buyers exercised maximum leverage. The cost of this policy misstep is not abstract — it is being counted per kilogram, by 600,000 smallholder farmers.

This brief applies tax incidence theory, price transmission economics, and distortionary tax analysis to assess likely impacts on farmer welfare and sector competitiveness. It concludes that the levy's design — structured on value rather than volume — contains a structural flaw that penalizes quality, rewards mediocrity, and is already driving buyers toward Kenya's competitors.

Background and Context

Kenya is the world's third-largest tea producer and the largest exporter of black CTC tea, accounting for approximately 22% of global black tea exports. In 2025, the sector posted a total marketed value of Ksh 218.79 billion, with export earnings of Ksh 186.91 billion — representing approximately 16.3% of national export revenue. Over 600,000 smallholder farmers, organised primarily through the Kenya Tea Development Agency (KTDA), depend on tea as their primary income source. The industry supports an estimated 7 to 10 million livelihoods across the full value chain.

It is in this context — an industry under simultaneous pressure from geopolitical market disruptions, currency headwinds, and oversupply — that a cluster of new tax measures must be evaluated. The question is not whether the government has the right to levy taxes; it unambiguously does. The question economics requires us to answer is: who actually bears the cost, and what are the unintended consequences on the sector's global competitiveness and farmer welfare?

Taxes and Levies

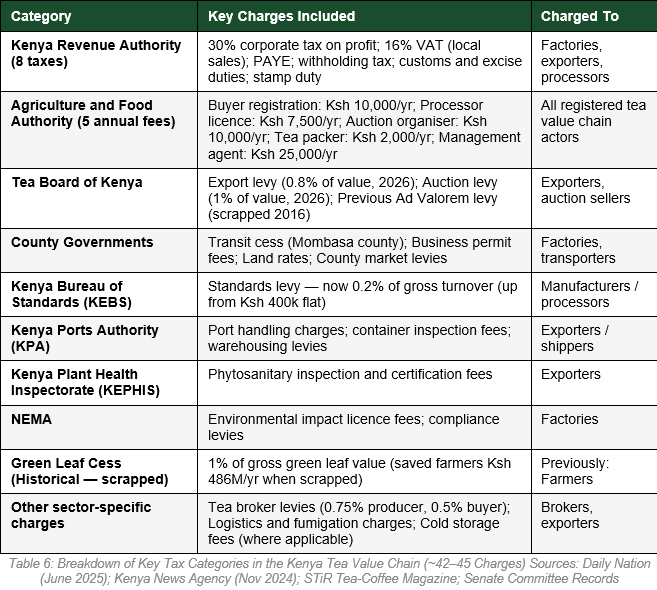

Taxes & Levies In Tea Value Chain

The sector already navigates 42 to 45 distinct taxes and levies across its value chain — a figure acknowledged by Kenya's own Agriculture Principal Secretary and debated in the Senate as recently as June 2025. These span eight KRA taxes (including 30% corporate tax and 16% VAT), five AFA annual licence fees, county government levies, KEBS compliance fees, KPA port charges, KEPHIS inspection fees, NEMA charges, broker levies, auction levies, and Mombasa county transit cess.

Previous Plan to Reduce Them

The government's own stated goal, prior to introducing the 2026 levies, was to reduce this burden. Introducing new levies against that commitment requires justification of the highest order.

The 0.8% Export Levy: Legal Intent vs. Economic Reality

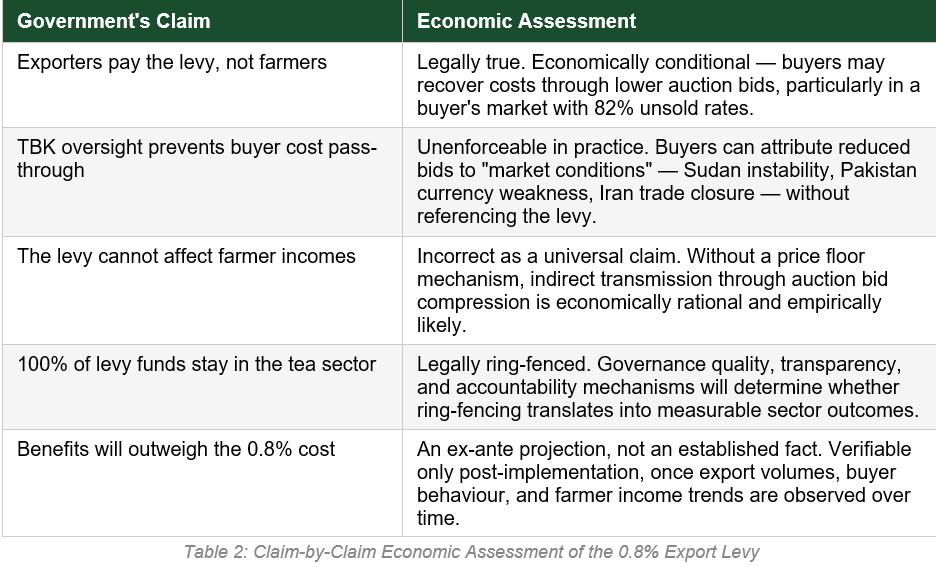

The levy, introduced under the Tea Levy Regulations, 2026 (Legal Notice No. 56 of April 1, 2026), took effect on May 1, 2026. Tea Board of Kenya Chairman Ndungu Gathinji confirmed the rate is 0.8% of auction value, while CS Mutahi Kagwe stated explicitly that the levy "will not burden farmers" as it is payable by exporters and importers. The Tea Board targets annual collections of Ksh 1.2 billion (approximately USD 9.3 million).

To be distributed as follows

- • 50% to a farmer income stabilisation fund

- • 20% for research and development via the Tea Research Institute of Kenya

- • 15% for regulatory functions through the Tea Board of Kenya (TBK)

- • 15% for infrastructure maintenance via county governments

- The stated objective — funding market diversification, global branding, factory modernisation, and road infrastructure — is legitimate. The mechanism chosen to pursue it is not.

The Economic Reality: Tax Incidence Theory

Public finance economics distinguishes between statutory incidence — who is legally required to remit a tax — and economic incidence — who ultimately bears the reduction in real income. These are not the same, and a century of empirical research, anchored by the work of economists Arnold Harberger and James Mirrlees, has established that legal obligation and economic burden routinely diverge.

Applied to the Kenyan tea auction, the mechanism works as follows: a buyer charged 0.8% of purchase value has two rational options — absorb the cost (compressing profit margins) or recover it by bidding slightly lower at auction. The incentive to pursue the second option is powerful in a market where Kenya exports 94% of its tea in unbranded bulk form and where buyer alternatives — Rwanda, Burundi, Uganda — are available on the same auction floor.

The Market Has Already Responded — and Not in Kenya's Favour

Economic theory predicts buyer adjustment. Market data, as of the first week of May 2026, confirms it has begun.

Reporting by Daily Nation (Anthony Kitimo, May 9, 2026) documents that within days of the levy taking effect, traders at the Mombasa auction actively shifted procurement toward Rwandan and Burundian teas instead of Kenyan lots. In a single week, KTDA alone paid over Ksh 450,000 in levy charges. At a session where only 18.14% of the 7.14 million kilograms on offer was bought — meaning 82% went unsold — buyers hold near-total market power. The incremental cost of the 0.8% levy, on top of Kenya's already-higher benchmark prices, is sufficient to tip sourcing decisions toward cheaper regional alternatives.

In Perspective

- On a standard 30,000 kg lot of Kenyan tea priced at USD 2.11/kg, the 0.8% levy adds approximately USD 510 in additional cost. That is sufficient — in a glutted auction with 82% unsold rates — for a cost-conscious buyer to choose Burundian tea instead. Kenya produces Africa's best tea. We should not be making it easier for buyers to justify choosing someone else's.

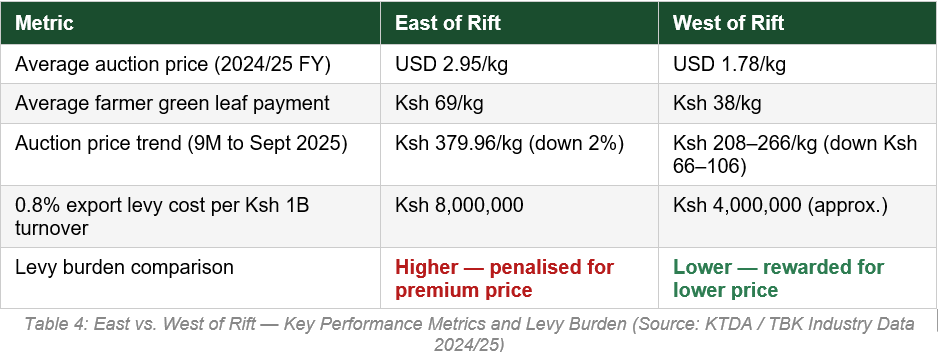

East of Rift Factories Are Paying a Premium for Excellence

A deeper structural flaw in the levy's design has received insufficient attention: it is structured as a percentage of auction value, not of volume. This creates an asymmetric burden across Kenya's tea-producing regions that is economically perverse and commercially damaging.

Tea grown in the East of Rift Valley — the Mt. Kenya belt covering Murang'a, Nyeri, Kirinyaga, Embu, Meru, and Kiambu counties — commands materially higher auction prices than West of Rift teas from Kericho, Nandi, Bomet, Kisii, and Nyamira. This premium reflects genuine quality differentials driven by altitude, climate, and agronomic discipline.

The consequence is already visible in buyer behaviour. Buyers sourcing teas for blending, for whom price is a primary variable, now have a financial incentive to tilt procurement toward West of Rift lots where the levy's absolute cost per kilogram is structurally lower. East of Rift factories — producing Kenya's most competitive, highest-value teas — face compressed demand and depressed bids. Not because their quality has declined. Because the levy has made them relatively more expensive to buy.

Equality

- Standard economic policy design prescribes that taxes should be neutral with respect to behaviour governments wish to encourage. A value-based levy that imposes a heavier burden on premium quality achievement creates a perverse incentive structure precisely when the sector needs to upgrade, invest in value addition, and defend its global premium positioning. A volume-based levy — a fixed shilling amount per kilogram exported — would distribute the burden neutrally across all producers and eliminate this distortion entirely.

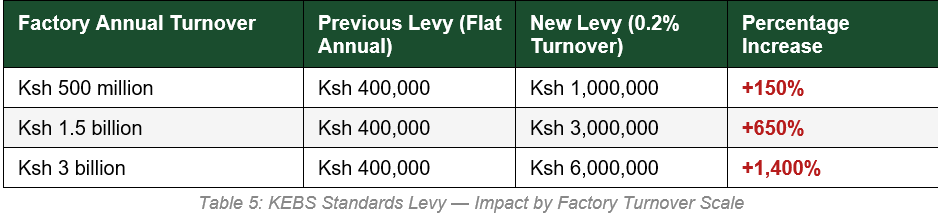

The KEBS Standards Levy: A 650% Cost Escalation Disguised as a Compliance Fee

While the export levy has attracted public debate, a second significant cost escalation has entered the sector with considerably less scrutiny. The KEBS Standards Levy, previously charged at a flat rate of Ksh 100,000 per quarter (approximately Ksh 400,000 annually regardless of factory size), has been revised to 0.2% of gross annual turnover.

Unlike the export levy, where incidence is debatable, the economic destination of the KEBS cost increase is clear: it lands directly on the factory. Every additional shilling in factory operating costs that cannot be recovered through higher tea prices reduces the net proceeds available for farmer bonus and second payment distributions. For a mid-sized factory operating on the thin margins characteristic of the KTDA model, a Ksh 2.6 million increase in annual compliance costs is not an abstraction — it is real money subtracted from what farmers receive at the end of the year.

No transition relief has been announced. No phased implementation has been offered. The escalation is immediate and total.

The 42 Taxes: What Kenya's Tea Farmers Already Carry

For the avoidance of doubt, the approximately 42 to 45 taxes and levies already operating in the tea value chain are not hypothetical. They have been catalogued in parliamentary proceedings, acknowledged by the Agriculture Principal Secretary, and reported extensively in the financial press. They span the following categories:

This is the environment into which the 2026 levies have been introduced. The National Treasury CS John Mbadi confirmed that a review of all 42 taxes was under consideration as recently as mid-2025. The decision to introduce additional levies prior to completing that review — and before publishing any Regulatory Impact Assessment — represents a significant governance gap that Parliament and the public deserve to scrutinise.

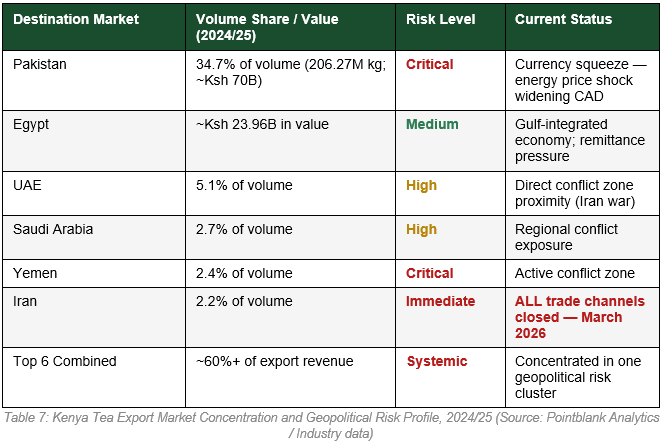

Market Concentration: The Structural Amplifier of Every Levy Burden

No tax analysis of Kenya's tea sector is complete without addressing the market structure that amplifies the damage any poorly designed levy causes. Kenya's export portfolio is characterized by dangerous concentration.

The US-Israel military offensive on Iran (March 2026) has closed Kenya's Iranian market entirely — a market where tea accounted for over 90% of bilateral trade. Pakistan, our single largest buyer at 34.7% of export volume, faces currency depreciation as Gulf energy prices pressure its current account. Analysis published by Pointblank Analytics estimates that a 10% contraction in Pakistani purchases would remove approximately Ksh 7 billion from the sector annually. A 20% contraction removes Ksh 14 billion. These scenarios are within the range of current conditions.

The Inherent Risk

- Market concentration and tax burden interact multiplicatively. In a diversified export portfolio, a new 0.8% levy is absorbed across many buyer relationships — no single buyer's attempt to pass the cost backward is decisive. In Kenya's concentrated structure, where 35% of volume flows through one buyer facing its own economic pressure and 60% through a geopolitical risk cluster, the seller's negotiating position is structurally weakened. Buyers know we need them more than they need us at this moment. That asymmetry is the exact environment in which levy pass-through to farmers is most probable.

What the Government Has Done Right — and Where the Contradiction Lies

This analysis does not dispute the government's commitment to the tea sector. Several interventions represent credible, evidence-based policy and deserve unambiguous acknowledgment:

The Interventions

- • Fertilizer subsidies: Fertilizer subsidies have directly reduced smallholder production costs, improving per-unit margins on green leaf delivery.

- • Infrastructure investment: Infrastructure investment in tea-growing regions — road rehabilitation, factory upgrades, and rural electrification — reduces operational costs and improves market connectivity.

- • Packaging tax exemption: The 2026 exemption of import duties on tea packaging materials directly supports value-addition and domestic branding, lowering the cost of producing packaged, branded tea for export.

- • KTDA governance reforms: Ongoing KTDA governance reforms aim to improve transparency and the farmer's share of final auction value. KTDA's target of 40% value-added exports under the ChaiGold brand is a credible structural ambition.

- • Farmer earnings target: The government has set an ambitious target of Ksh 100 per kilogram of green leaf for farmers by 2027, and this goal commands respect as a policy anchor.

Where is the Problem?

The problem is coherence. Farmer income is determined by the net of two forces: revenues and costs. The government has made genuine progress on cost reduction. The simultaneous introduction of new levies undermines that progress by adding costs on the revenue side of the same equation.

What Makes a Farmer Wealthier ?

- A farmer does not become wealthier because production increases alone. A farmer becomes wealthier when a larger share of the final market value of tea reaches the farm gate. Policy coherence demands that cost-reducing measures are not simultaneously undermined by contradictory revenue-compressing tax impositions. The Ksh 100/kg target for East of Rift farmers is incompatible with a value-based levy that compresses the auction premium their quality commands.

Policy Recommendations

Based on the analysis in this brief, the following policy corrections are recommended, listed in order of urgency:

Policy corrections Recommended

Redesign the Export Levy as a Volume-Based (Per-Kilogram) Charge — Immediately

The 0.8% value-based levy should be converted to a fixed per-kilogram charge applied uniformly across all exported tea regardless of auction price. This eliminates the quality distortion, distributes the burden neutrally, preserves incentives for premium production, and removes the mechanism by which East of Rift factories are penalised for excellence. It also removes the buyer's ability to exploit value differentials when choosing between Kenyan and regional teas.

Restore a Minimum Reserve Price at the Mombasa Auction

The government's assurance that farmers cannot be affected by the levy is only credible in the presence of a guaranteed minimum auction price that prevents buyers from transmitting costs backward. Kenya scrapped its price floor in 2024. Without its restoration, the protection offered to farmers is a promise, not a mechanism. A minimum reserve price or auction floor should be reinstated as a precondition for the levy's continued operation.

Provide Transition Relief on the KEBS Levy Escalation

The 650% increase in KEBS levy costs for mid-sized factories should be subject to a phased implementation over three to five years, with an annual cap on the percentage increase permitted. No factory should absorb a multi-million shilling compliance cost escalation in a single regulatory cycle without transitional support.

Publish a Full Review of the 42–45 Tea Value Chain Taxes Before Introducing Further Levies

The Agriculture Principal Secretary committed to reviewing the 42 existing taxes in late 2024. That review must be completed, published, and translated into a rationalization roadmap before any new levy is introduced. A sector burdened with 42 taxes does not need new additions — it needs consolidation, simplification, and elimination of duplicative charges.

Treat Market Diversification as a National Policy Priority Funded by Levy Revenue

Kenya's 60%+ revenue exposure to a single geopolitical risk cluster is a national fiscal vulnerability. A meaningful share of the Ksh 1.2 billion targeted annually from the export levy should be contractually committed to market development in China, Eastern Europe, Southeast Asia, and domestic value-added consumption — with independently verified outcomes reported publicly.

Conclusion

Kenya's tea sector is absorbing multiple simultaneous shocks: a geopolitical disruption closing its Iranian market and squeezing its Pakistani one; an oversupplied global auction where 82% of lots go unsold; a structural quality premium under pressure from cheaper regional competitors; and now a compounding tax burden introduced without floor price protection, without a completed impact assessment, and without the rationalization of 42 existing levies that was promised before these new ones were imposed.

The 0.8% export levy is not wrong in its objectives. Funding market promotion, research, and infrastructure is legitimate. The mechanism — value-based rather than volume-based — is structurally flawed. It penalises the factories that produce Kenya's best tea, it rewards complacency over quality, and it has already triggered buyer flight toward Rwanda and Burundi. The market is delivering its verdict in real time.

Parliament has both the authority and the mandate to correct this. Factory directors, farmer cooperative leaders, and county representatives have the standing to demand it. And the courts — given the documented questions about the levy's gazettement process — have the jurisdiction to scrutinise it.

The 600,000 farmers who pick Kenya's tea are not asking for special treatment. They are asking for a tax system that does not punish them for growing the best tea in Africa. That is a reasonable ask. It deserves a serious answer.

Tax & Levies Tranasfer

- Statutory incidence is who writes the cheque. Economic incidence is who bears the cost. In Kenya's tea sector today, those are not the same person.

Editorial Note

This analysis represents expert commentary on economic policy and political developments. All information has been fact-checked and cross-verified from reliable sources. The views expressed are based on professional analysis and independent research.